Here's how to know — and what to do about it.

Most business owners set up their 401(k) plan, hand it to a provider, and trust that it's running fine. And it might be. But if you haven't reviewed your plan's fees and investment lineup recently, you may be paying more than you should — and unknowingly exposing yourself to legal liability in the process.

BY THE NUMBERS — CALLAN 2025 DC SURVEY

IF NO ONE HAS COMPLAINED, DOES IT MATTER?

Yes — and here's why. Your employees are unlikely to notice if their retirement account is quietly losing ground to unnecessary fees. But plaintiffs' attorneys might. Lawsuits against 401(k) plan sponsors have grown steadily over the past decade, and they're no longer limited to large corporations. Mid-sized plans are increasingly targeted, often because their sponsors assumed they were too small to matter.

When a lawsuit or Department of Labor audit happens, the question isn't just "were the fees high?" It's "did you follow a documented, prudent process to review them?" Sponsors with a clear paper trail are in a very different position than those who can't show they ever looked. The good news: building that trail isn't complicated — it just has to actually happen.

WHAT RESPONSIBLE PLAN GOVERNANCE LOOKS LIKE

✓ Keep your Investment Policy Statement current

Think of this as your plan's rulebook — it defines how you select and monitor investments. 86% of plan sponsors reviewed theirs in 2024. Without an up-to-date IPS, your investment decisions have no documented framework behind them, which is one of the first things an auditor or plaintiff's attorney will look for.

✓ Benchmark your fees against comparable plans

You don't need the lowest fees in the industry — you need fees that are reasonable for what you're getting. That means periodically comparing your plan's costs against similar plans in terms of size and structure. Sponsors who can't show they've done this are more vulnerable in litigation, even if their fees turn out to be competitive.

✓ Know what you're really paying — including hidden costs

The number on your fund's expense ratio isn't the whole story. Your recordkeeper may be receiving revenue sharing payments from fund companies, or earning fees from managed accounts and rollover services. Over half of plan sponsors now evaluate these sources of indirect compensation — and if you're not, you may be significantly underestimating your plan's true cost.

✓ Review your default investment funds

Most participants never actively choose their investments — they end up in your plan's default fund, typically a target date fund. These funds now hold the majority of assets in most plans, yet over 1 in 5 sponsors haven't reviewed their default fund lineup recently. Are the fees competitive? Is the investment approach appropriate for your workforce? These questions deserve a real answer.

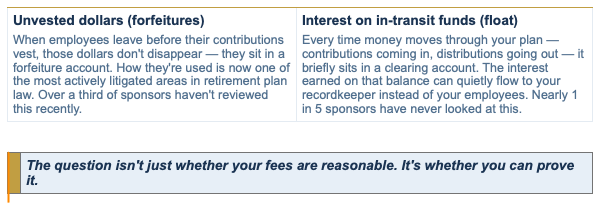

⚠ Check what happens to unvested contributions when employees leave

When a worker leaves before they're fully vested, their unvested employer contributions go into a forfeiture account. How you use those dollars — to reduce your own contributions, cover plan expenses, or let them sit — is now one of the most actively litigated areas of retirement plan law. Yet only 65% of sponsors reviewed their forfeiture practices last year.

⚠ Find out who's keeping the interest on in-transit funds

Every time money moves through your plan, it briefly sits in a clearing account. The interest earned on those funds — called float — can quietly flow to your recordkeeper rather than your employees. It's a small number that adds up, and nearly 1 in 5 plan sponsors have never looked at it.

TWO AREAS MOST SPONSORS OVERLOOK ENTIRELY

A 401(k) plan is one of the most valuable things you offer your employees — and one of the most significant legal responsibilities you carry as a business owner. When it's well-managed, it's a genuine competitive advantage: a signal that you're invested in your people's long-term financial security. When it's not, it's a liability that could surface at the worst possible time.

The standard for what "well-managed" means is rising. More plan sponsors are formalizing their governance processes, benchmarking fees, and documenting their decisions. That's the new standard — and plans that aren't keeping pace are accumulating risk, even if nothing has gone wrong yet.

The good news is that getting your plan in order is more straightforward than most business owners expect. A structured fee and governance review typically takes a few weeks, surfaces concrete findings, and leaves you with documentation that protects you going forward. For most plans, it also results in a better deal for employees — lower costs, a cleaner fund lineup, or both.

At Gambit Capital Management, we work exclusively with business owners and executives. We know your 401(k) is one of many things competing for your attention — so we make the process easy. You tell us about your plan; we do the analysis and come back with clear, actionable findings. No jargon. No pressure. Just an honest answer to the question: is your plan working as hard for your employees as it should be?

HERE'S HOW IT WORKS

Get a free 401(k) fee review

It takes 30 minutes and costs you nothing. Most business owners walk away with at least one concrete finding — and peace of mind that their plan is on solid ground.

Schedule your free consultation → gambitcm.com/contact